The recently concluded World Economic Forum conference at Davos which was attended by luminaries from all over the globe had an interesting theme for this year namely “Resilient Dynamism”. This has been arrived at based on the balance needed between the two counter forces in the world economy: viz. ‘Agility and Dynamism’ needed to grab the huge transformational opportunities that exist AND ‘risk resilience’ which is needed in the wake of the imminent risks emanating from the problems ailing the economies in different parts of the world.

There is an increased probability of “Black Swan” events happening in future and the two main reasons for this unpredictability and foggy vision are ‘mounting debts and fiscal deficits in several economies’ and ‘lack of inclusive growth’. The Indian IT firms which are epitomes of corporate governance and modern management practices have to support the cause of inclusive and sustainable growth failing which the long term survival of the organizations will be in question. What is important is not only maximization of value creation to the shareholders but also making an impact on the society and environment at large. The WEF theme of “Resilient Dynamism” is very relevant to the Indian IT firms as well.

The Feb 2013 issue of HBR has an interesting article on the “Top 100 CEOs for 2012” which ranked the CEOs of 3000 global companies on the basis of the performance of their respective firms during their tenure as the CEO. Surprisingly none of the CEOs of the Indian IT firms figure in this list. The ranking was done based on the net value creation done by the respective firms, which was measured by the delta change in the market capitalization of the firm during the tenure of a CEO (after adjusting for industry and country specific fluctuations). This goes to show that while the Indian IT industry was much appreciated for its transformation of the Indian economy and for bringing India onto the global radar, none of these firms created extraordinary returns for their shareholders in the period under consideration. The CEOs of other Indian firms like ITC, ONGC, Reliance, Airtel and L&T figure in the HBR Top 100 CEO list for 2012.

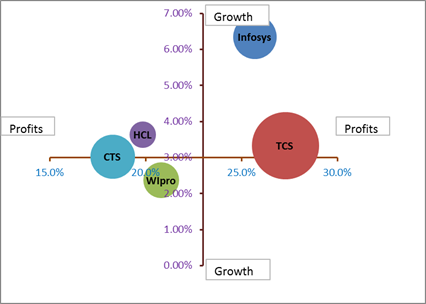

In the ‘Value Creation’ Quadrant below, I have attempted to classify the Top 5 Indian IT firms on two axes, viz. Profitability (operating profits as a % of revenues) and Growth (QoQ growth for the current quarter) and the scenario looks as follows:

1. HIGH PROFITS and HIGH GROWTH: Infosys

2. HIGH PROFITS and MODERATE GROWTH: TCS

3. LOW PROFITS and MODERATE GROWTH: Cognizant

4. LOW PROFITS and MODERATE GROWTH: HCL

5. LOW PROFITS and LOW GROWTH: Wipro

The bubble scatter of the Top 5 Indian IT firms on the twin axes of Profitability and Growth is as follows with the ‘size of the bubble’ being an indicator of Quarter revenues:

Value Creation Quadrant for Q3, FY13

Value Creation Quadrant for Q2, FY13

Like I mentioned in my last quarter’s analysis report when comparing the Top 5 IT firms, we need to lay specific emphasis on the “net value creation” to the shareholders in dollar terms and not worry too much about the growth rate or the profitability % in isolation. The market however does not just look at the cumulative value creation to shareholders at a point in time or the total value creation in a quarter. The market value is based on the net present value of the anticipated future value creation to the shareholders over a longer time horizon which is function of both the growth rate and profitability. The market typically assumes that the companies with rapid growth rates are expected to create more value over a longer time horizon and hence place a premium on these firms. However if such rapidly growing firms show even minor drop in the growth rate the impact on their market valuation is very steep. Apple is a classic case in point whose market valuation crashed as it could not convince the markets of continuity in its growth rates despite a record growth of 18% QoQ in the current quarter and consistently good performances in the preceding quarters as well.

From the above perspective let me attempt to give my point of view on how the potential value creation in absolute dollar terms for these firms might look like in future.

While TCS is much lower in the quadrant in terms of growth, its profitability is slightly higher than Infosys and it also ranks first in terms of the absolute operating profits as its revenue base is large. TCS has moved down in the quadrant over the previous quarter. TCS will however be probably ahead of Infosys in terms of sustainable value creation in the long run assuming the current growth and profitability rates to remain as they are.

Infosys is in the Top Quadrant and has the highest growth rate and the second highest profitability. It has improved its position substantially from the last quarter’s quadrant. If it can maintain its profitability at these levels or even if its growth tapers to the level of TCS in the coming quarters it is still poised to create a very good value in the long run. It is ranked second in terms of absolute operating profits in dollar terms in the current quarter.

Cognizant has a low margin and its operating profit in absolute terms is much lower and unless it performs consistently at highest levels of growth in the industry the overall value creation will be much lower than that of TCS and Infosys. Also there will be significant fluctuations in its market value when its growth rate decreases as its profitability is low. Cognizant has moved down significantly in its quadrant position compared to its position in the last quarter.

HCL will come next in terms of the long term value creation based on its current performance and its position in the quadrant has almost remained constant.

Wipro might be the last in term of long term value creation despite its moving up the quadrant by a notch over the last quarter unless its growth rate improves and becomes more predictable. However in terms of the net value creation in absolute dollar terms it remains ahead of HCL in the current quarter.

For more detailed Financial Performance Analysis for this quarter please click here

Please feel free to send in your valuable feedback/comments on my analysis…